Tuesday, January 31, 2012

Monday, January 30, 2012

Sunday, January 29, 2012

travel insurance to avoid

ms teo siew hoon's letter; captioned: travel insurance to avoid was published in the st forum online on saturday.

in her letter, ms teo recounted her claim's experience with general insurer, chartis on her damaged luggage which took almost 4 weeks (add another 2 weeks after her claim submission) for her to be informed to obtain a quotation to repair her luggage and send it to her insurer.

as a comparison, ms teo cited that if she had made a similar claim for damaged luggage to an airline, the latter would probably pick up the luggage, assess the repair and inform quickly whether the luggage would be repaired and returned or replaced.

she ended by expressing her hope that other insurance companies do not make their customers wait the way chartis has done.

my comments:

as a financial planner and a traveler myself, i can empathise with ms teo over her damaged luggage and also her claim experience with chartis.

many of my clients take up travel insurance, which is probably the smallest priced component of any vacation for peace of mind.

i am not trying to discount or minimise ms teo's feedback but in my experience, travel insurance claims like damaged luggage are very much the norm, rather than the exception and insurers usually admit and pay such claims speedily, after due diligence of course.

but take a step back and look at the big picture in terms of the comprehensiveness of what a travel policy covers and not what ms teo has chosen to focus on how an airline will deal with her damaged luggage.

after all, as the saying goes, one swallow does not a summer make.

Saturday, January 28, 2012

whole-of-life alternative to universal life

an article with the abovementioned title by ms genevieve cua in the weekend edition of the business times caught my eye.

in her article, ms cua touched on some basics of whole life and universal life products. she also said that the appeal of universal life lies partly in the flexible premium financiing and rightly pointed out the latter calls up a different set of risks of which one caveat is that as the client ages and a scenario should rates fall to the minimum crediting rate, it may be possible that the death benefit may decline and clients may be asked to top-up the premium to ensure the policy does not lapse. on this, ms cua pointed out that some universal life products do have a 'no-lapse' guarantee option but this comes with an additional premium.

the article singled out tokio marine life insurance tm legacy vip, a single premium participating whole of life plan with an immediate cash value, making it possible to take a policy loan after inception of the plan.

mr odd haavik of charles monat associates said that he liked what tokio marine life insurance is doing and their history of never cutting bonuses is a good selling point and reckons that this product is appropriate for a high net worth client so long as they are comfortable with the less transparent nature of the whole-of-life product as compared to universal life.

my comments:

Friday, January 27, 2012

Thursday, January 26, 2012

cashing in on the lunar new year?

during the first 2 days of the lunar new year, many consumers (including myself and my family) would have discovered that stalls levied a 'premium' for food and drinks purchased during this festive period.

just to cite an example, hot drinks like coffee and tea has been hiked to $0.90 to $1.20 instead of the usual $0.70 to $0.90. and simple meals like a bowl of noodles cost $3.50, or $0.50 more than the usual $3.00 during the non-festive period.

however, in an article by the free local tabloid, today, it was reported that even though the lunar new year (public holidays) are over, prices have remained high when prices are expected to return to normal when stalls resume business after the holidays.

one example is ltn food village at east coast road where 3 of the 10 stalls put up signs to indicate higher prices. another one is food xchange coffeeshop where drink prices were also raised by between $0.10 and $1.00.

some of the stallholders responded that suppliers had increased their prices also driving costs up by as much as 20% this month.

my comments:

whether justified or not, i feel consumers can still exercise their choice of whom they wish to do 'business' with during the lunar new year holidsay but i must admit the choices are rather limited during this time as many stalls remained closed.

on the other hand, our insurers do not and have never indulged in the practice of driving prices of insurance products up during this festive season or any other time to cash in on the timing of the season.

during my entire 15 years in the financial industry, i have noticed a clear trend of the repricing of insurance products to the benefit of the consumer and the community. this is particularly true of term assurance, both level term and mortgage reducing term assurance products.

even more recently, the cpf board has repriced their home protection scheme premium rates (effective january 01, 2012) to be much lower and in sync with the insurance industry resulting in huge savings of as much as 12% for cpf members.

and i'm sure that in an environment of high inflation (it was 5.2% in 2011), u will agree with me that every penny counts.

Wednesday, January 25, 2012

the dragon year, in more ways than one

i read the abovementioned article with great interest by mr toh yong chuan, senior correspondent, published in today's edition of the straits times.

he started off by illustrating that the word, dragon denotes firstly prosperity or something that is grand.

he cites the local stock market using the example of the sti which ended the year 2000 (the last dragon year) at 1,927 points and market capitalisation then was $417.8 billion. at the end of 2011, the sti had gone up to 2,646 points and market capitalisation at a much higher $716.3 billion.

other statistics:

singapore's gdp was $165.2 billion in 2000 to $284.6 in 2010

trade nearly doubled from $470 billion to $902 billion

singapore got bigger from 683 sq km to 712 sq km

population grew from 4 million to 5 million

literacy from 92.5% to 95.9%

life expectancy from 78 years to 81.8 years

more doctors, from 14 per 10,000 people to 17 per 10,000 people

more nurses, from 40 per 10,000 people to 57 per 10,000 people

more government spending on health from #301 to $808 per person

mobile phone subscriptions from 606 to 1,436 per 1,000 people

more driving cars from 92 to 111 cars per 1,000 people

more watching pay tv from 255,000 to 802,000 subscriptions

newspaper circulation from 1.38 to 1.53 million

more borrowing books (and other materials) from public libraries from 24.5 to 33.2 million

and also on a positive note, crime fell from 720 to 650 per 100,000 people.

on the negative side, he said that there is a difficulty faced by those in the bottom 20% of the income ladder because the incomes of the bottom fifth stood still, from $12,00 to $1,400 growing only 0.3% after taking inflation into account. this group would have fared worse if not for government programmes like workfare.

he also pointed out the worrying trend of families under strain in terms of marriages falling apart. while there have been more marriages from 22,561 in 2000 to 24,363 in 2010, more are ending in divorce which rose from 5,160 to 7,405.

and there are more elderly staying at old folk's homes from 6,022 to 9,755 in 2010 when they should be spending their golden years with their families.

the author ended by reminding us not to take for granted we will always be prosperous, not to be deaf but listen to those around us and give a lift to those who feel caged.

my comments:

after one chinese zodiac cycle, it is noteworthy to know that the majority of the statistics are positive for our tiny red dot nation and the vast majority of our population.

but many of the negatives are also real, with the income of the bottom 20% standing still, more marriages but more ending in divorce, and more elderly living in old folk's homes compounded by the fact that life expectancy is constantly growing.

and these are all real life issues and they have everything to do with financial planning and the 4Ws of wealth management.

the good news is, it is never too late to plan, but rather it is usually failure to plan which is almost like planning to fail. and so long as u are alive and well, the years ahead can be better than u think or imagine but only if u do something about it and the key is, the earlier the better.

Tuesday, January 24, 2012

the world's first trillionaire?

my first blog to kick off the lunar new year is on wealth or lots and lots of it in the form of the world's first trillionaire who is known as mr kamal ashnawi.

many people probably would have heard of mr carlos slim helu, the mexican mega tycoon with an estimated worth of US$63.3 billion and acknowledged as the richest person in the world.

but who is mr kamal ashnawi?

Kamal Ashnawi, 42 years old was born in Tanjung Malim, Perak, Malaysia and is the president of sierra petroleum.

according to sources as reported by the malaysian media in a news conference, mr kamal ashnawi said his net worth was $6.4 trillion, and yes, u are reading right, it's trillions and expressed in numerical form, it is $6,400,000,000,000 which is equivalent to approx RM20 trillion ringgit.

my comments:

wow, imagine the number of digits of the wealth of this person and if true, may be accorded the title of the world's very first trillionaire.

i do not know whether there are any other trillionaires in the world but we can certainly boast of the highest number of millionaires in our tiny red dot nation.

even if u are not a millionaire yet, taking up a seven digit insurance policy* should have the effect of the creation of a large estate or if u like, leaving a huge legacy for your chosen beneficiary/ies and or adopted charities.

and an insurance policy, specifically a term policy is perhaps the most cost-effecitive solution with this end in mind.

*terms and conditions apply.

Monday, January 23, 2012

happy chinese new year 2012

wishing each and everyone, a blessed chinese new year running over with good health, abundance, prosperity and success in all areas of your life.

Sunday, January 22, 2012

Saturday, January 21, 2012

Friday, January 20, 2012

Thursday, January 19, 2012

financial stability top list of insurers' concerns: geneva association

in a newly published study by the geneva association*, it lists out the top concerns facing the insurance industry in 2012 which includes:

a. current global financial instability

b. concerns over governmental management of natural catastrophic risk and

c. the demographics of dealing with ageing socities.

the secretary general and managing director of geneva association, mr patrick m. liedtke on the current financial crisis said that:

"no other topic has worried nation states around the world more persistently in 2011 than the question of global financial stability."

on claims for natural catastrophes that struck in 2011, mr liedtke said that it is:

"by far the most expensive year on record for natural catastrophe insurance with estimated claims reaching some US$380 billion. even given some variation from current loss estimates, 2011 will turn out to be nearly two-thirds more expensive than 2005, the next most expensive year (US$220 billion). but the issue here is not only one of claims and payouts - it is one of human tragedies and loss."

on the concern regarding the demographics of dealing with ageing socities, and while it is a positive that people are living longer, this poses a dilemma for the governments of the countries they live in, which is in turn worsened by the financial crisis.

on this, mr liedtke said:

"in light of the current state of many sovereigns and their finances, they do so facing greater uncertainty than other retirees in several decades. doubts over heavily indebted states' ability to provide social security have increased. volatile returns from many private sector investment products have eroded confidence in pension provisions and retirement planning. yet, individuals continue to seek stable streams of income that will afford them a decent standard of living beyond their working years."

In conclusion Liedtke urged both society and politicians to “grasp the nettle and face up to the inevitable implications of these long standing challenges. Given the role of the insurance industry and its ability to provide long-term stability, it has the potential to be a significant part of the solution to this problem. This is a great opportunity for all involved. In 2012, insurers should raise the profile of this issue and be the leading private sector counterparty to help governments develop a credible and sustainable way forward.”

*from wikipedia on the geneva association:

The Geneva Association is the leading international insurance “think tank” for strategically important insurance and risk management issues.

The Geneva Association identifies fundamental trends and strategic issues where insurance plays a substantial role or which influence the insurance sector. Through the development of research programmes, regular publications and the organisation of international meetings, The Geneva Association serves as a catalyst for progress in the understanding of risk and insurance matters and acts as an information creator and disseminator. It is the leading voice of the largest insurance groups worldwide in the dialogue with international institutions. In parallel, it advances—in economic and cultural terms—the development and application of risk management and the understanding of uncertainty in the modern economy.

my comments:

Tuesday, January 17, 2012

Monday, January 16, 2012

Sunday, January 15, 2012

Saturday, January 14, 2012

Friday, January 13, 2012

Thursday, January 12, 2012

Wednesday, January 11, 2012

Tuesday, January 10, 2012

ns man dies after finishing 2.4km run

it is really heart wrenching to learn that a young man in his prime fainted and then died after completing the mandatory 2.4km ippt run during in-camp training which was widely reported in our local media today.

in a statement from the defence ministry said that 28-year-old cpl Li Hongyang, a security trooper from the 62nd Combat Service Support Battalion, fainted after completing his 2.4km run at 8:38am which happened at the kranji camp III where cpl li was undergoing in-camp training.

my comments:

surely our hearts and prayers go out to the family and relatives of the late cpl li who's gone too soon.

i remember my reservist days and when notified to attend in-camp training has always been accompanied by much anxiety over completing the 2.4km run which is the so-called gold standard to clear because the other physical exercises like chin-ups, push-ups, broad jump, etc were considered to be a walk-in-the-part for young men in their prime.

looking back, i thank God for clearing each ippt test without having to go through the mandatory re-calling for an additional in-camp stint should any reservist fail their ippt.

i suppose in today's point of reference, the thingy to do is to prepare for the tests and more importantly, a health screen prior to putting oneself through physical tests where the body has to respond to additional demands from everyday living.

and from the prespective of wealth protection, the clause on exclusion of pre-existing conditions is central to the contract where any claim is admitted and paid because modern day living is perhaps filled with more stress than before.

and doctors will readily tell u that stress is a link in almost every disease and so on and so forth.

therefore, do be gently reminded again that an insurance contract hinges on the material information in the application form and any incomplete disclosure may render the policy to be void and no benefit payable.

Monday, January 9, 2012

Sunday, January 8, 2012

Saturday, January 7, 2012

axa sells hong kong-based ipac advisory firm

recently, there was an article with the same captioned headlines which was reported in the international adviser* by ms helen burggraf, deputy editor of the publication.

the artilce said that Ipac chief executive Rainbow Pan declined to confirm that Ipac was on the block, saying it was company policy not to comment on “speculation [and] rumours”.

Ipac specialises in providing high-end, fee-based advice to wealthy expatriates as well as to a growing number of local residents in all its jurisdictions but the firm has never produced a profit for Axa since it was acquired in 2002 for A$250m.

*International Adviser

International Adviser provides up to the minute news, tools and professional resources for Independent Financial Advisers in the UK, Europe, Middle East and Asia Pacific regions.

my comments:

the artilce said that Ipac chief executive Rainbow Pan declined to confirm that Ipac was on the block, saying it was company policy not to comment on “speculation [and] rumours”.

Ipac specialises in providing high-end, fee-based advice to wealthy expatriates as well as to a growing number of local residents in all its jurisdictions but the firm has never produced a profit for Axa since it was acquired in 2002 for A$250m.

*International Adviser

International Adviser provides up to the minute news, tools and professional resources for Independent Financial Advisers in the UK, Europe, Middle East and Asia Pacific regions.

my comments:

Friday, January 6, 2012

ntuc-income: repricing of growth plan

this is really fresh from the oven because we have just received an urgent email notification from ntuc-income (at approx 6pm):

Dear Valued Partners,

Over the last few years, interest rates have declined significantly. 12 months fixed deposit rates are now hovering around 0.4% p.a. compared to 0.9% p.a. 5 years ago. Similarly, 5-year Singapore government bond yields have declined from 3.2% p.a. 5 years ago to 0.9% p.a. today. As a result, it is becoming increasingly challenging to design and price this type of single premium savings plan, such as our Growth Plan. As you know, many of our fellow competitors areno longer selling such plans.

We will be _replacing_ thecurrent version of *Growth Plan (GRL3)*with a new revised version. Details of the new version of Growth Plan to replace the current version will be made in a separate announcement. The new Growth Plan will be available from 09 January 2012.

*Last day of submission for existing **Growth Plan (GRL3)**will be _09 January 2012_ at the close of business day. Application Form and BI bearing date after 09 January 2012 will _not_ be considered for **Growth Plan (GRL3)**.*

There are some letters sent to policyholders with maturities due in February 2012, inviting them to reinvest. For these cases, _if application comes in by 09 Jan 2012_, we can make an exception to issue these policies on maturity date. For maturities beyond February 2012, the reinvestment will have to be under the new version of Growth Plan.

Kindly note that all *Growth Plan (GRL3)* applications pending for payment or documentation must be completed and issued by 31 January 2012, otherwise they will be considered as ‘Not Taken Up’ (NTU).

We recognize the demand for single premium savings planand its place in the financial plans of our valued customers. We will continue to make available such plan to our customers as long as we are able to do so sustainably.

Thank you for your kind attention.

Warmest Regards

Financial Advisers, Sales Division

FA Hotline: (65) 9746 2663

www.income.com.sg

my comments:

to be really honest, it comes as no surprise to me that the current growth plan* will be repriced wef january 09, 2012.

if we look at a similar class, non-anticipated, participating single premium endowment product, it is a really near extinct animal, with tokio marine life insurance tm wealth enhancement (enrich) plan still left on the shelf.

but ntuc-income growth is probably pretty accessible to everyone, open to cpfis-oa, cpfis-sa, srs and cash payment. what's more, entry level is a very low single premium of just $5,000 whereas tokio marine life insurance tm wealth enhancement (enrich) has a much higher single premium requirement of $20,000 and is definitely not open to cpfis-oa and cpfis-sa as well.

furthermore, ntuc-income growth is also open to medically sub-standard lives.^

^terms and conditions apply.

my guess is the new revised version of growth will see the guaranteed cash value on maturity to be lower and the non-guaranteed cash value, headed north.

anyway, i do not want to jump the gun and shall await with bated breath, the new growth plan to be rolled-out this coming monday, january 09, 2012.

^mtuc-income growth plan is a non-anticipated participating single premium endowment plan.

and benefits at a glance:

■Flexible investment term

■Guaranteed1 returns on your principal sum upon maturity

■Yearly bonus2 based on financial results of the Life Participating Fund

■Payout of sum assured plus accumulated bonuses2 or cash value, whichever is higher, in the event of Death or Total and Permanent Disability (TPD before the age of 65)

■Payout of 2 times the sum assured plus accumulated bonuses2 in the event of an accident resulting in Death or Total and Permanent Disability (TPD before the age of 65)

IMPORTANT NOTES:

1 The guaranteed returns are payable only if the policy is held until maturity, on the condition that no policy alterations or related transactions have occurred during the entire policy term

2 Bonus rates are not guaranteed and the actual maturity benefits may vary according to the future performance of the Life Participating Fund.

3 Policy term of 11 to 20 years are only available for CPFIS and SRS and not available for cash investment.

4 The projected maturity benefit are based on a level of bonus rates, deemed supportable based on the assumption that the Life Participating Fund earns a projected return of 5.25% per annum in the future.

This blog is for general information only and is not a contract of insurance. The precise terms, conditions and exclusions of this plan are specified in the Policy Contract.

You should seek advice from a qualified adviser if in doubt. If you choose not to, you will have to take sole responsibility to ensure that this product is appropriate to your financial needs and insurance objectives.

Buying a life insurance policy is a long-term commitment. An early termination of the policy usually involves high costs and the surrender value payable may be less than the total premiums paid

Thursday, January 5, 2012

study shows memory loss can start as early at 45

in a reuters article which highlighted the findings of a 10-year study of more than 7,000 british government workers show that loss of memory and other brain function can start as early as age 45*, which contradicts previous notions that cognitive decline does not begin before age 60. and this poses a big challenge to scientists looking for new ways to stave off dementia, researchers said.

*the research findings were published in the British Medical Journal, alongside an editorial by Francine Grodstein of the Brigham and Women's Hospital in Boston, who described the results as convincing.

to pinpoint the age at which memory, reasoning and comprehension skills start to deteriorate is imperative because drugs are most likely to work if given when people first start to experience mental impairment.

the research team led by Archana Singh-Manoux from the Center for Research in Epidemiology and Population Health in France and University College London found a modest decline in mental reasoning in men and women aged 45-49 years.

Archana Singh-Manoux said in a telephone interview that they were expecting to see no decline, based on past research.

Archana Singh-Manoux also said:

"It doesn't suddenly happen when you get old. That variability exists much earlier on. The next step is going to be to tease that apart and look for links to risk factors."

the participants were assessed three times during the study, using tests for memory, vocabulary, and aural and visual comprehension skills.

and over the 10-year period, there was a 3.6 percent decline in mental reasoning in both men and women aged 45-49 at the start of the study, while the decline for men aged 65-70 was 9.6 percent and 7.4 percent for women.

since the youngest individuals at the start of the study were 45, it is possible that the decline in cognition might have commenced even earlier.

factors affecting cardiovascular function -- such as obesity, high blood pressure, high cholesterol and smoking -- are believed to impact the development of Alzheimer's and vascular dementia through effects on brain blood vessels and brain cells.

most research into dementia tend to focus on people aged 65 and over. In the future, scientists will need to devise long-term clinical studies that include much younger age groups and may have to enroll tens of thousands of participants, she said.

and Archana Singh-Manoux added:

"One way to deal with this "major challenge" might be to use computerised cognitive assessment tests, rather than face-to-face interviews, although more research is still needed on this approach."

my comments:

wow, so what was thought to be conventional acceptance that memory loss does not begin until one reaches his/her sunset years has been stirred by this latest findings conducted over a 10 year period.

i know several individuals who has cognitive impairment and they can be classified as being healthy without risk factors like obesity, high blood pressure and high cholesterol. neither are these people smokers and furthermore, they are not in the 'over-the-hill' category because one was in her early 40s who needed a 24/7 full-time care giver and her beloved husband to carry out everyday functions which we take very much for granted.

it is indeed sobering to digest the latest findings that memory loss can start as early as in one's prime of life but it is even more heart wrenching to lose loved ones to mental impairment.

for those of us who are not on the wrong side of the equation, thank God there are tools and solutions to take care of that eventuality (which hopefully will not happen) and engaging a competent financial planner is surely the first step in the right direction.

Wednesday, January 4, 2012

aia singapore pte ltd

with effect from january 01, 2012, aia, in a media release announced that aia in singapore will be known as aia singapore pte ltd with the insurance business in singapore being successfully transferred from a branch to a singapore-incorporated and a wholly-owned subsidiary of american international assurance company, limited. aia singapore also announced its inaugural AA- financial strength rating with stable outlook from rating agency, standard & poor's.

the ceo of aia singapore, mr tan hak leh said:

"having been in operation as a branch office in singapore for over 80 years since 1931, the transfer of our business to a singapore-incorporated company - aia singapore - is a very significant milestone for us. it reinforces our commitment to meeting the protection and savings needs of singaporean families across generations and we will continue to introduce innovative products and deliver quality service to help singaporean families bridge their underinsurance gap."

my comments:

existing aia policyholders have been informed of the transfer in september 2011 and all existing policy contracts with american international assurance company limited have been automatically transferred to aia singapore. with the transfer now formalised, all aia policyholders will continue to enjoy the same terms and conditions of their insurance policies.

we are proud to be part of the aia story and i have noticed a discernable change in the company's more customer-centric focus in many areas especially in the enhancement of existing products and in the development of new products (akan datang). and to quote one product, aia secure term plus has been re-priced (since november 2011) to be super competitive amongst similar class products in the market place.

we wish aia singapore pte ltd every success in the years to come.

Tuesday, January 3, 2012

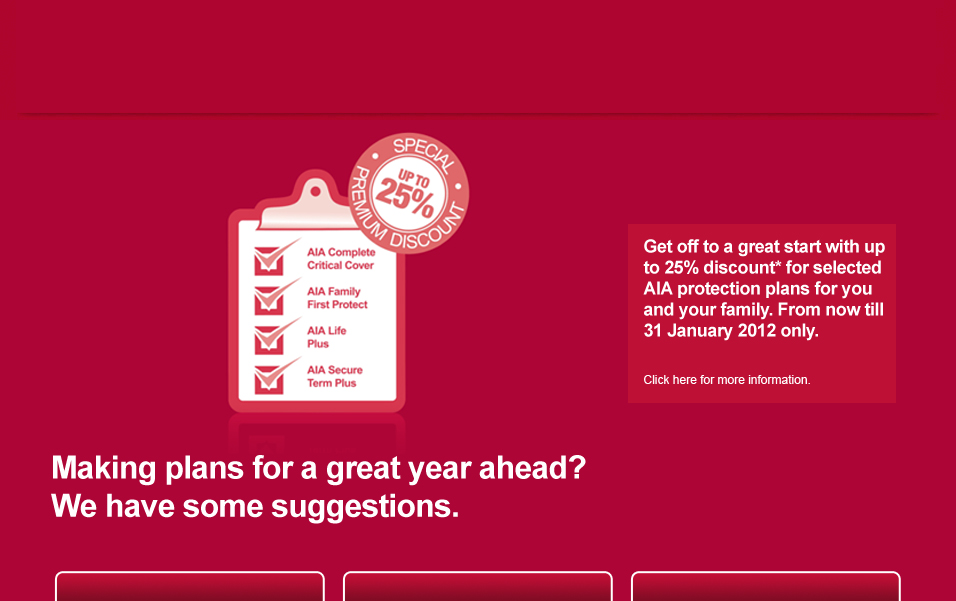

aia promotion

i shall kick-off my very first blog entry for 2012 with some good news from aia.

aia is currently having a promotion for 4 of their champion products:

a. aia complete critical cover

b. aia family first protect

c. aia life plus and

d. aia secure term plus

where there is a special premium discount of up to 25% for taking up any one of the abovementioned products.

the promotion period is from january 01 - 31 january 31, both dates inclusive, except aia secure term plus for which the promotion period of december 12, 2011 to january 31, 2012, both dates inclusive, applies.

the 25% premium discount is limited to aia complete critical cover as well as any and all optional riders purchased with it and plans eligible for the 20% discount are limited to aia family first protect, aia life plus and aia secure term plus as well as any and all optional riders purchased with such policies.

but do take note the 20% or 25% premium discount rates (as applicable) only apply to your first year premiums for annual mode of premium payment. however, if u choose to pay your premiums, monthly, lower rates of premium discounts will apply and your 3rd and 4th months' premiums in the first policy year will be waived.

the other promotion comes in the form of the early bird lunar dragon lucky draw open to all singapore citizens and residents who are aged 21 and above collectively, the 'eligible persons' and each, an eligible person). the promotion period for the draw is from january 01 to 22, 2012, both dates inclusive.

a chance to win a lunar dragon 24k gold ingot worth $988.00 will be allocated to each eligible person for every eligible plan applied and incepted within the promotion period (plans must be effective by march 31, 2012).

the draw will be conducted on february 16, 2012 at aia tower, 1 robinson road, singapore 048542 at 3.00pm (or such other date or time or at such other venue as may be determined by aia) and 3 winning eligible persons will be selected at random by such means and methods (which may be manual or computerised) as aia may determine in the presence of an external public accountant.

each winner will be entitled to only one prize, regardless of the number of wins.

important notes:

all insurance applications are subject to underwriting and acceptance by american international assurance company, limited (before january 1, 2012) or aia singapore pte ltd on or after january 01, 2012.

my comments:

Sunday, January 1, 2012

happy new year

as we reflect on the year that was 2011, here's moi wishing one and all, good health and an even more successful, peaceful, joyous and prosperous 2012 filled with abundance and all the good things in life.

God Bless.

Subscribe to:

Posts (Atom)